How Fader works

Fader is a research tool that screens the S&P 500 and a set of liquid ETFs for stocks that just made an unusually large, statistically extreme one-off move, and then prices the premium-selling trade that fades (bets against) that overreaction — selling puts after a sharp drop or calls after a sharp pop, on a ~1–2 week horizon. Every number is computed from real fetched market data (prices, the live options chain, implied volatility, news); Fader never invents figures.

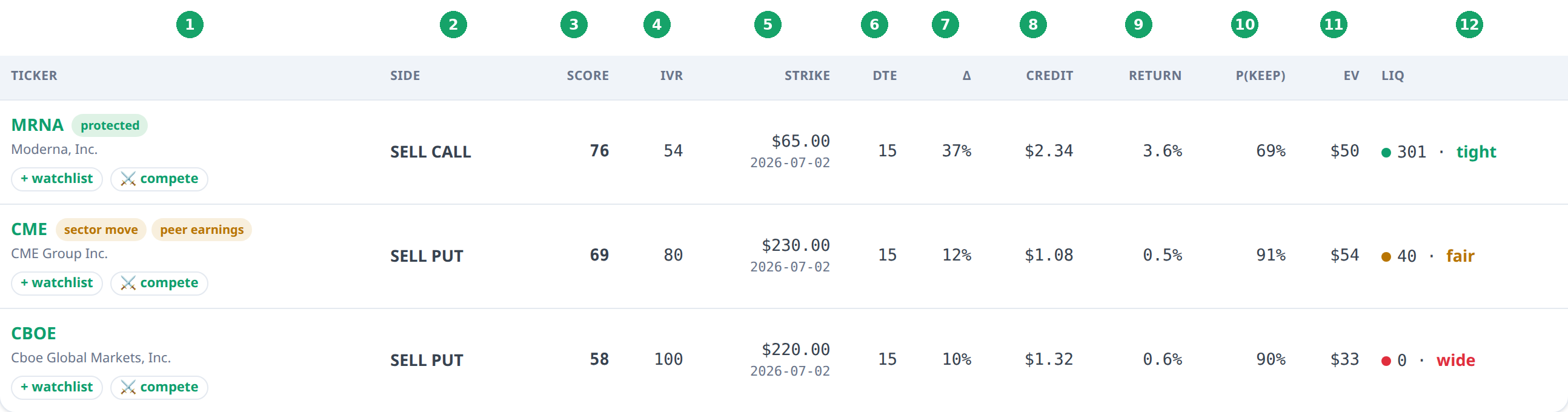

Reading the results table

The numbers above point to each column, explained below.

| 1. Ticker | The stock or ETF symbol. A small ·ETF marks a fund; ·DJI marks a Dow-30 member. |

| 2. Side | What Fader suggests selling: SELL PUT after a sharp drop, SELL CALL after a sharp pop — you're fading (betting against) the overreaction. |

| 3. Score | The fade score, 0–100: how attractive the trade is — it blends the overreaction with the real options edge (IV-rank premium, chain EV, liquidity, structure), a direction-aware trend adjustment, and a sector-relative-move adjustment (a move that's mostly sector-wide is penalised). A ranking heuristic, NOT a probability. See “How the fade score works” below. |

| 4. IVR | IV Rank (0–100): where the option's current implied volatility sits versus its own past year. Higher = options premium is rich relative to this name's normal. Example: IVR 80 means IV is near the top of its 1-year range, so you're being paid a fat premium to sell. |

| 5. Strike | The real, listed strike price Fader suggests SELLING — chosen about 1 standard deviation out-of-the-money from the live options chain. The date under it is the expiration. |

| 6. DTE | Days to expiration of the suggested contract. Fader keeps this short (about 1–2 weeks) — this is a quick premium-collection strategy. |

| 7. Δ (Delta) | The option's delta from the chain ≈ the market's rough probability it finishes in-the-money, shown as a percentage. A lower delta means further out-of-the-money = safer for a seller. Example: Delta 20% ≈ the market pricing roughly a 20% chance the option finishes in-the-money. |

| 8. Credit | The premium you collect per share, taken at the mid of the bid/ask. Multiply by 100 for dollars per contract. Example: Credit $1.20 = $120 collected for one contract. |

| 9. Return | The premium yield for the trade if the option expires worthless = credit ÷ collateral, over the ~1–2 week hold. Deliberately NOT annualized (annualizing a 2-week trade overstates it). Example: Collect $2 against a $100 strike ≈ 2% for the period. |

| 10. P(keep) | Fader's model probability that the option expires worthless and you keep the full premium — a realized-volatility Monte-Carlo estimate with no drift. An estimate, never a guarantee. Example: P(keep) 85% = the model thinks ~85% odds you keep the whole premium. |

| 11. EV | Expected value per contract = the credit you collect MINUS the payout expected under realized volatility. Positive EV means the premium looks rich versus the move that's actually likely — that's the edge Fader is hunting. Example: EV +$35 = on average, after accounting for the realistic chance of a loss, the trade is worth about $35 per contract. |

| 12. Liq (Liquidity) | How easily you could actually trade the option: open interest (number of contracts outstanding) and a tight / fair / wide rating of the bid/ask spread as a % of the credit. The spread is rated on an ETF or single-name scale (ETFs quote tighter, so they're held to a stricter bar). A small coloured dot shows the rating — green = tight, amber = fair, red = wide. Tight spread + healthy open interest = easy to fill. Example: 1,500 · tight = 1,500 contracts open and a tight spread (easy to trade). 40 · wide = barely any open interest and a wide spread (avoid). |

| 13. Flags (beside the ticker) | Short tags shown next to each symbol so you can read a setup's quality at a glance — amber = caution, green = favorable. trend = the move sits inside an established up/down trend (continuation / falling-knife risk); sector move = much of the move is the whole sector (systematic — it may persist rather than revert); peer earnings = a correlated same-sector name reports inside the holding window and could gap this stock; earnings = the stock's own report is near or inside the window; thin liq = the best sellable strike is below Fader's normal open-interest floor; at-level / exposed = where your short strike sits versus the nearest heavy-volume price level; protected = the short strike sits beyond a level (favorable); buy → $X / short → $X = no tradeable options, so an equity-fade plan instead. Triggers with negative expected value (no edge) or a thesis-break news headline are moved into a collapsed “screened out” section below the table — shown for transparency, never hidden, because the score's own EV calc already flags them as having no edge. |

| 14. Earnings | Earnings-date awareness. A premium sale should EXPIRE BEFORE the next earnings report — you don't want to hold a short option through the announcement jump. Fader shortens the suggested expiry to land before earnings when it can; if earnings is too soon to fit (or the move itself IS a post-earnings reaction), the name shows an earnings flag and is pushed down the ranking (and skipped by the paper-trader). Example: “earnings in 4d (too soon to fade)” = the report lands inside the holding window and there's no earlier expiry — better to wait. ETFs show no earnings flag because they have no single-company report. |

| 15. Defined-risk version | An optional safer structure shown on each trade: instead of selling a naked option, you also BUY a further-out option as a hedge (a vertical spread). This caps your worst-case loss to a known dollar amount, in exchange for collecting a bit less premium. Shown with its net credit, capped max loss, EV and breakeven. Example: Sell the $95 put / buy the $90 put: you collect less than the naked $95 put, but your loss can never exceed the $5 width minus the credit — no surprise tail. |

How the fade score works

The fade score (0–100) ranks how attractive the trade is — not just how dramatic the chart looks. It blends the overreaction with the real options edge. It's still a ranking heuristic, not a probability or a guarantee.

The yes/no trigger is a separate gate: a name only fires if it had a large move (≥4% in a day or ≥8% over 5 days) that was statistically extreme (≥2σ vs its normal volatility) with no thesis-breaking news. The score then ranks the names that fired.

The score adds up five ingredients, then adjusts for the trend:

| Ingredient | Max | What it rewards |

|---|---|---|

| Overextension | 25 | How many standard deviations the move was — the size of the overreaction we want to fade. |

| Premium richness | 25 | The option's IV Rank — how rich the premium is versus this name's own past year. Higher = you're paid more to sell. |

| Edge (EV) | 30 | The real expected value from the live chain (credit minus the loss expected under realistic volatility) plus annualized return. Positive edge is the whole point; negative-EV setups score low here. |

| Liquidity | 10 | Open interest + a tight bid/ask spread — can you actually get filled without giving up your edge. |

| Structure | 10 | Whether your short strike sits beyond a heavy-volume price level (an auction floor/ceiling) rather than in open air. |

The trend adjustment (direction-aware)

A trend isn't good or bad on its own — what matters is whether your trade runs with the bigger trend or fights it. The idea: fade the short-term spike, but don't fight the prevailing trend.

| Your trade vs the bigger trend | Example | Adjustment |

|---|---|---|

| With the trend (fading a counter-trend blip) | Sell puts on a dip within an uptrend; sell calls on a bounce within a downtrend. | +8 reward |

| Against the trend | Sell puts while the stock is in a downtrend; sell calls while it's in an uptrend. | −12 |

| Falling-knife grind | A sustained, one-directional slide (no real shock to fade). | −25 |

The trigger and the score are separate. A name can score low and still be a valid trigger — it just carries trend risk or thin/negative edge — so it's shown (not hidden) for you to judge. And a high score is not a recommendation: always read it alongside the EV, P(keep), Liquidity and Flags columns.

How to use the scan — a read-the-results playbook

This is an educational walkthrough of how to read a Fader row — what the columns and flags mean and how the rules Fader's own paper-trader follows are derived from them. It describes one research approach for context; it is not advice, not a recommendation, and not a suggestion that you place any trade. What (if anything) you do with it is your own decision.

- Start with the edge, not the drama. The real edge is the premium being rich, not the size of the move. Look at IVR and EV first — high IVR + positive EV is a genuine edge. A dramatic drop with low IVR and negative EV is a trap.

- Lean toward puts; be picky on calls. Selling puts harvests the normally-overpriced put skew (a tailwind); selling calls doesn't, and a bounce can squeeze. Take put setups more readily; hold call setups to a higher bar.

- Respect the flags — especially earnings. A red earnings flag means the trade spans a report, or the move is the earnings reaction — skip or wait. Mind the trend and news flags too, and treat no edge (negative EV) as a near-hard skip.

- Check liquidity before you act. Only trade tight or fair rows in the Liq column (green or amber dot); avoid wide (red). If a name shows no suggested strike, that's Fader saying it's untradeable — don't force it.

- Favor ETFs / indices for steadier results. Their premium is more reliable than a single stock's, and they carry no earnings-gap risk. Treat single-stock triggers as the higher-variance plays.

- Default to the defined-risk version. Click a ticker → Trade tab → the Defined-risk version caps the worst case to a known dollar amount (you collect a bit less), whereas a naked short carries an open-ended tail. Which structure fits depends entirely on your own capital, risk tolerance and situation.

- Size small, spread out. Several small positions beat one big bet — the edge is noisy per stock. Size a little bigger on the best setups (high IVR + EV), smaller on the marginal ones, never all-in on one.

- Have an exit plan. Taking profits early (Fader's bot buys back at ~50% of the credit) and knowing your exit matters more than win rate. Whether “take 50%” beats “let it ride” is exactly what the Track record measures.

The one-line version: the setups Fader's paper-trader favours are high-IVR, positive-EV, tight/fair liquidity, clean flags, preferably a put or an ETF, defined-risk and small — that's the rule set in a sentence. You can watch fader-bot to see whether those rules actually pay off. This is a description of the tool's own approach for education, not a recommendation to you.

Hypothetical performance. Backtests, win rates, and paper-trading results shown here are model-based and hypothetical — no real money is traded. Hypothetical and simulated results have inherent limitations, do not reflect actual trading, and do not guarantee future results.

Sector & peer-earnings awareness

Fading works best on a stock-specific overreaction that snaps back. It works worst when the move is really the whole group repricing — a sector rotation or a correlated peer's report — because those tend to persist, not revert. Two checks keep Fader honest about that distinction:

| Sector-relative move | Every move is split into the part driven by the stock's sector (systematic) and the part that's stock-specific (idiosyncratic), by comparing the stock to its SPDR sector ETF. When most of a drop is the whole sector moving together — software sold off with the group, say — the setup gets a sector move flag and a score penalty, because a sector theme can keep going. A move the sector didn't share is a cleaner, more fadeable overreaction. |

| Peer earnings | A short-vol trade should expire before the stock's own report — but tightly correlated names move together, so a same-sector peer reporting inside your holding window can gap your position too. Fader checks the forward earnings calendar and flags peer earnings when a correlated name reports soon. Browse the full earnings calendar for the next three weeks while you size a trade. |

Both are descriptive signals computed from public prices and the public earnings calendar — Fader reports what the data shows and you decide. Not advice.

What's new — sharpened against the volatility literature

We reviewed four standard professional texts on volatility/option trading and used them to tighten Fader. Each change below names why and where it comes from. The throughline: the real edge is the variance premium (implied vol is usually richer than the move that actually happens), and the job is to harvest it without getting killed by the tail.

| Change | Why | Source |

|---|---|---|

| 📅 Earnings awareness | A short-vol trade should expire before the next earnings date — holding a premium sale through an earnings jump is exactly the risk you don't want. Fader now shortens the expiry to land before earnings, and flags / skips names where earnings is too soon. It also avoids fading a move that is a post-earnings reaction, because those tend to keep going (momentum), not reverse. | Bennett, Trading Volatility §1.2; Augen, The Volatility Edge ch.7; Sinclair, Positional Option Trading ch.5 (PEAD) |

| Defined-risk version | Every trade now also shows a spread version that caps the worst-case loss. A naked option keeps the whole premium but carries an unbounded tail; buying a protective wing removes that tail (and the skew) for a little less credit. | Sinclair ch.8; Natenberg, Option Volatility & Pricing |

| Puts ≠ calls | Selling OTM puts harvests the equity put skew, which is normally overpriced — a structural tailwind. Selling OTM calls doesn't, and fading a pop risks a squeeze. The score now nudges accordingly. | Bennett §1.4 |

| Liquidity gate | A suggested strike must have real open interest and a live bid — gated on liquidity, not on the quoted spread (single-name options are legitimately wide even when liquid). Stops Fader from suggesting strikes whose “mid” credit can't actually be collected. | Bennett (index vs single-stock premium); Sinclair |

| Edge-scaled sizing & more names | The paper-trading validation now sizes each trade by its edge (a quarter-Kelly-style scale, capped), spreads across more names, and leans toward ETFs/indices where the variance premium is more reliable — instead of three equal single-stock bets. | Sinclair ch.9 (fractional Kelly); Bennett (index premium) |

| Equal-risk cap (new) | A hard cap on the collateral behind any one name: a stock whose single contract would exceed the cap is skipped rather than taken as an outsized 1-lot. Stops one high-priced ticker from quietly becoming most of the book's P&L and risk. Results are also reported per dollar at risk, not just in raw dollars. | our 2026-06-30 results review |

| Don't fade a rising tape (new) | Selling calls is penalised — and in a clearly risk-off / melt-up tape, vetoed — when the name itself or the whole market is trending up. Fading momentum is the side that lost money; the put side is left alone. | our regime backtest; Bennett §1.4 |

| Stops & rolls (new) | A loser is now stopped early (bought back once the option roughly doubles) instead of riding to a breach, and a tested short can be rolled — buy it back and sell one further out — but only when it can be done for a net credit into a strike that still keeps a majority chance of expiring worthless. Otherwise it's closed for a defined loss. | tastytrade roll discipline; Sinclair ch.9 |

| Faster scorecard (new) | Every call now also settles on a fixed ~2-week horizon in parallel with at-expiry, so a real keep-rate exists weeks before the monthly options expire. | our 2026-06-30 results review |

These books are about professional volatility trading and assume an experienced reader. Fader applies their ideas; it is still a research tool, not advice, and the figures are Fader's own estimates from live data.

How the paper track record is run

Fader keeps an honest, self-contained paper track record so you can see whether the signals actually pay before risking real money. Here's exactly how it's set up — no black box.

| What it trades | After each daily scan it sells the top few positive-EV setups (puts that harvest the rich put skew, leaning toward ETFs/indices), skipping anything spanning an earnings report. Size is edge-scaled (quarter-Kelly), small, and spread across names. |

| No broker — self-tracked | We don't route to a paper broker. For thinly-traded single-name options a broker's live quotes are noise (they once “stopped out” a $220 put for a big loss while the stock sat at $243, never near the strike). Instead each sale is logged at the chain mid minus a small slippage haircut — a realistic fill, never a phantom one. |

| How positions are valued | Every open trade is marked daily with a Black-Scholes model off the underlying stock price (clean data), its remaining days, and realized volatility — so the unrealized P&L is honest, drawdowns and all. |

| How it's managed | Decisions are made on the stock, never the option quote: take profit when the model mark reaches 50% of the credit; stop a loser once the option roughly doubles; roll a tested short further out when (and only when) it can be done for a net credit into a high-cushion strike; otherwise exit if the stock trades through your breakeven. At expiry it settles on the real closing price. |

| Two books, side by side | It tracks the managed book (take 50%) against a hold-to-expiry shadow on the same picks — a live head-to-head on whether taking profits early beats letting them ride. |

Paper money, not advice. The figures are Fader's own model estimates from live data.

Hypothetical performance. Backtests, win rates, and paper-trading results shown here are model-based and hypothetical — no real money is traded. Hypothetical and simulated results have inherent limitations, do not reflect actual trading, and do not guarantee future results.

Fantasy Trader — the leaderboard

Fantasy Trader is Fader's friendly paper-trading contest. It's separate from your watchlist: the watchlist is just for tracking trades you want to watch; Fantasy Trader is where you enter trades to compete on the leaderboard. Paper money, not advice.

| How to enter | On any flagged row hit ⚔️ compete (or open a ticker → Trade tab). Choose your structure and size, then enter. The list is scanned once a day and emailed — everyone competes off the same daily triggers. |

| Naked or defined-risk | Pick naked (sell the option, keep the full credit, larger max loss) or a defined-risk spread (buy a protective wing, keep less credit, a capped max loss). The panel shows your credit collected and max loss live as you change structure and contracts. |

| Sizing | Choose how many contracts. Size counts — a bigger position swings your P&L (and your risk) more. Both you and the bot are scored by actual size. |

| Live fills | Each entry transacts at the live mark — priced off the underlying the moment you enter (the same model used to value every position), so it mimics a real fill and your P&L starts flat. No broker. If the market is closed when you enter, it stays pending and fills at the next open, so nobody games stale after-hours prices. |

| Add or sell anytime | Enter more positions whenever you like, and Sell a position to close it and lock in its P&L (also filling at the next open if the market's closed). Removing an entry (✕) just deletes it without recording a result. |

| 🤖 fader-bot | The auto-trader competes too, scored off its own paper book — so there's always a benchmark to beat. |

| Scoring & ranks | Every position is marked with the same model as the track record (credit collected minus the option's current value, priced off the underlying). The leaderboard shows total P&L, average per pick, best pick, win rate, and open/closed. Pick a nickname on the leaderboard. |

| Weekly reset | The board resets every week (Mon–Sun) so anyone who joins mid-contest competes on a level field. A pick scores in the week you opened it and stays there — its P&L floats while open and freezes when you sell, so closing an old position still moves that week's total up or down. Each pick is tagged with its week (📅) so you always know which week a sell affects. Switch between This week, a past week, or All-time with the picker on the leaderboard; your all-time total is always kept too. |

Where the data comes from

Prices and implied volatility are pulled live from public market-data sources; the suggested strikes, credits, deltas and open interest come from the real options chain; news headlines are scanned for thesis-breaking events. Fader computes every figure itself and shows “—” rather than guessing when data is missing.

Is this financial advice?

No. Fader is for research and education only — it is not financial advice, not a recommendation, and not an offer to buy or sell any security. Options trading carries substantial risk of loss. See the Terms of Use and Privacy Policy.

Have a question Fader's data can answer? Open the chat bubble (bottom-right) and ask the Fader Assistant.